Flood Re: a missed opportunity for sustainable flood risk management?

Posted on 8 Apr 2016 in Commentary

The government and the insurance industry have recently launched Flood Re, a scheme that aims to make home insurance affordable to those living in a flood risk area. But that alone does not solve the problem, writes Swenja Surminski. These efforts should be accompanied by improvements to land-use planning, as well as by steps to build stronger flood defences, as these are some of the changes that will provide a more comprehensive management of flood risk.

After years of negotiations, the government and the insurance industry have agreed to set up Flood Re, which offers flood insurance cover for high risk households, with fixed premiums (ranging from £210 to £540) dependent on council tax banding. The not-for-profit pool is funded by these premiums in addition to an annual levy taken from all insurance policy-holders, independent of their flood risk exposure, which is currently expected to be around £10.50 per policy, and will be imposed on insurers according to their market share. Premiums and levies will be reviewed every five years, with changes requiring the approval of the Secretary of the State.

Flood Re officially started its operations across the UK on 4 April 2016. Designed to secure affordable cover for properties at high risk of flooding, the flood insurance pool complements the current insurance market, where private insurers are offering cover against flood damage as part of standard home insurance policies. Government and industry present the scheme as a roadmap to future affordability and availability of flood insurance, but it is far from clear if and how Flood Re will help us to address the real problem: flood losses are rising, largely due to socio-economic trends such as urbanisation, more buildings in exposed areas, and failed land-use practices. Climate change is expected to exacerbate these risks, with surface water flooding, storm surges, and river flooding projected to increase in many areas across the country.

Keeping premiums affordable while pay-outs grow is difficult, and may lead to decreasing commercial viability for private sector insurance companies, or ever higher public liabilities. This can be seen in the United States, where the National Flood Insurance Program has been identified as one of the highest financial risks for the government. As highlighted in the recent Bank of England report on climate change, this could also cause the system in the UK to fail – with those providing cover walking away or those requiring insurance unable to pay as premiums become unaffordable.

For owners of homes built before 2009 and currently at high risk of flooding, Flood Re puts a cap on the rising costs of insurance. For those deemed to be at low risk, the levy means subsidising those in the pool. This mechanism is set to run for 25 years, after which Flood Re is designed to stop its operations, as set out in the supporting legislation. This is based on the assumption that over the next 25 years, flood risk will be managed well enough for insurance costs to go down so that no further intervention to keep premiums affordable will be needed. At the moment, there is no guarantee this will be the case.

The gap between affordable flood insurance and flood risk management

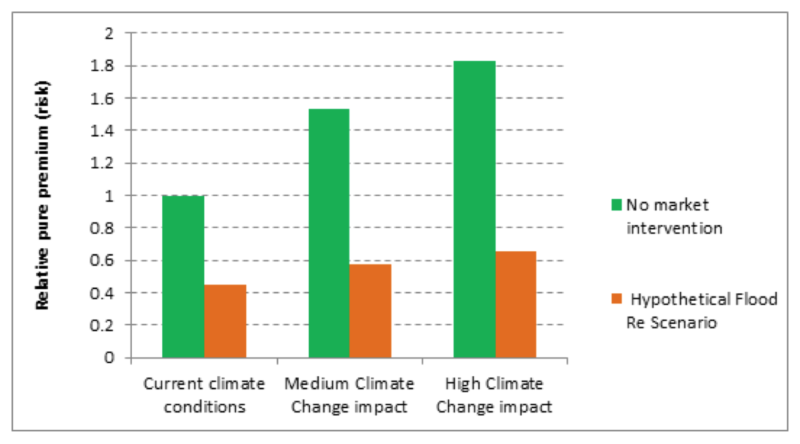

In its ‘transition plan’, Flood Re acknowledges that effective flood risk management is crucial to ensure the affordability and availability of flood insurance: if the losses from flooding are not reduced, we are likely to see a significant difference between the price of subsidised coverage through Flood Re and the technical risk price. Our research, highlighted in the Bank of England report, shows that climate change and socio-economic risk drivers are expected to widen the gap between ‘affordable’ flood insurance premiums and premiums that reflect the technical price of flood insurance (see Figure 1).

Figure 1. The Pricing Implication of Climate Change

Based on Jenkins et al. (2016), cited in Prudential Regulation Authority and Bank of England: The impact of climate change on the UK insurance sector (2015)

These issues were not fully taken into account during the design of Flood Re; in its current form the scheme will not help to address the underlying causes of flooding. Flood Re itself points out that it has no direct levers to influence flood resilience. The scheme is unlikely to impact the behaviour of those groups that will determine future risk levels: homeowners, national and local governments, developers and insurance companies. This is a missed opportunity. The failure to build incentives to increase resilience into the design of Flood Re could even have a detrimental effect on overall flood risk management. The scheme’s existence may reduce the urgency for government to prevent and reduce risks and also reduce incentives for home- and business-owners to invest in resilience measures i.e. it creates moral hazard.

A crucial component of making homes and businesses more resilient to flooding is raising awareness of the risks posed and of the options for managing them. Yet research by the Environment Agency shows that many homeowners who live on floodplains in the UK are unaware that they are at some risk of flooding, according to figures cited by the Committee on Climate Change. Hence, there is a need to utilise Flood Re to raise awareness and incentivise action.

Nevertheless, under the current proposal, Flood Re is ‘invisible’ to the households it covers. Those households covered by the scheme should be made aware in their policy documentation that they are benefitting from subsidised insurance cover and should be provided with information about their flood risk level and what measures are in place to protect them. Flood Re could also be used to offer incentives for households to increase their resilience to flooding. For example, we recommend that successful claims are made contingent on sensible resilience measures being taken as part of re-build. For incentives to be successful, they need to target those who can take action. In the case of insurance this could mean that more stakeholders need to be included in the development of new solutions, for example property developers, mortgage providers and local planning officials, who all determine if, where and how houses are being built, refurbished or repaired.

Flood Re buys time, but not sustainability

Of particular concern would be any extension of Flood Re to also cover new homes built since 2009. This would remove the only remaining resilience incentive that Flood Re can use – by not offering cover for new homes, it sends a signal to property developers and home-buyers to consider flood risk when building and purchasing homes, as subsidised flood insurance will not be available for the owners. Neither the UK government nor the insurance industry should hide behind Flood Re. All it does is buy us some time: it helps to alleviate the immediate pressure of rising flood insurance costs, but unless we utilise Flood Re to drive resilience, it is unlikely to be sustainable.

To achieve sustainability, the UK needs to develop a comprehensive strategy for flood risk management. The strategy should adopt a holistic approach, and include improving land-use and planning policy, increasing the resilience for the existing housing stock, and building stronger flood defences, alongside efforts to keep insurance affordable. The National Flood Resilience Review, launched by the government in December 2015, could be an important step towards the creation of such a comprehensive flood risk management strategy for the UK. We cannot afford another missed opportunity.