Shale gas: how does the hype stack up against robust analysis of the evidence?

Posted on 1 May 2012 in Commentary

A strident campaign has been mounted over the past couple of years to promote shale gas as a ‘game-changing’ new source of energy that can be extracted readily and in plentiful amounts, can reduce fuel bills, and can also help the UK to reduce its emissions of greenhouse gases.

For example, a report written for Lord Lawson’s Global Warming Policy Foundation by Matt Ridley, the science writer and former chairman of Northern Rock, suggested that a surge in the production and use of shale gas “may prove to be both the cheapest and most effective way to hasten the decarbonisation of the world economy”.

But how does this hype stack up against robust analysis of the evidence?

What is shale gas and ‘fracking’?

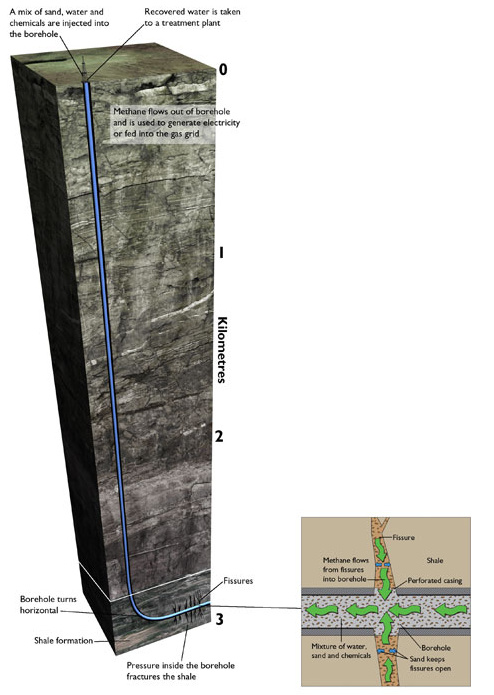

Shale gas refers to an unconventional source of methane which can be extracted from deposits of a fine-grained rock that is rich in organic material. Although shale deposits have been known for some time to contain large amounts of natural gas, they have been difficult to exploit because of the relatively impermeable nature of the rock. However, recent advances in drilling and extraction techniques have made such stores of natural gas easier to withdraw. In particular, the process of hydraulic fracturing, or ‘fracking’, can be used to shatter the rock with pressurised water to allow the gas to be extracted.

{kind=link}

Production and consumption of shale gas in the United States

Proponents of shale gas point to the United States, where annual dry production of natural gas increased by 14.0 per cent between 2006 and 2010 to 759.9 billion cubic metres, according to the Energy Information Administration (EIA). Much of the increase over this period has been achieved through horizontal drilling, combined with fracking, to boost the annual production of shale gas nearly fivefold to about 141.3 billion cubic metres in 2010).

The EIA estimates that there are 23,418 billion cubic metres of natural gas, equivalent to 36 years of current annual consumption, which are recoverable from shale in the United States using current technology. It has projected that annual dry production of shale gas could reach 384 billion cubic metres by 2035, growing from about 23 per cent of dry natural gas production to 49 per cent over the next 25 years.

However, the significant increase in supply over the past few years has been accompanied by weak demand in the United States, due to a combination of the economic downturn and relatively mild winter weather. Consumption of natural gas in the United States fell from 659.1 billion cubic metres in 2008 to 648.7 billion in 2009 before rising to 673.2 billion in 2010. The volume of imported natural gas as a percentage of supply also decreased from 16.7 per cent in 2007 to 13.1 per cent in 2010.

As a result of the increase in production and weakening of demand, the average price for natural gas at the well-head fell by more than half over 12 months from a high point in 2008, and was 63.7 per cent lower by January 2012. Spot prices for natural gas in the United States approached a 10-year low at the end of March 2012 due to continued high production levels, robust storage and weak demand arising from the mild winter (according to the United States National Oceanic and Atmospheric Administration, the traditional cold season in the United States between October and March in 2011-12 was the second warmest since records began in 1880).

The substantial reduction in the price of natural gas after its peak in 2008 has provided a cost advantage for gas-powered electricity generation plants over those fuelled by coal. The amount of electricity generated from natural gas reached a record 24 per cent by the end of 2010.

Impact of increased shale gas on greenhouse gas emissions in the United States

As gas is a more efficient source of fuel, the switch from coal also helped to reduce annual emissions of carbon dioxide from electricity generation in the United States by 214.5 million tonnes between 2008 and 2009. More than half of this reduction can be attributed to the switch from coal, driven by increased production of shale gas, according to Xi Lu and colleagues at Harvard University. As overall carbon dioxide emissions in the United States were 423.8 million tonnes, or 7.2 per cent, lower in 2009 compared with 2008, the switch from coal to gas may have been responsible for about a quarter of the overall cut in greenhouse gas emissions by 440 million tonnes of carbon-dioxide-equivalent that was recorded by the Environmental Protection Agency. It should be noted that overall carbon dioxide emissions in the United States increased by 205.9 million tonnes in 2010, primarily due to an increase in economic activity.

These facts provide a very different picture from that presented by Matt Ridley in an article in ‘The Times’ on 18 April 2012 where he wrongly suggested that the work of Dr Lu and colleagues show “the surprise fall in America’s carbon emissions – by 7 per cent in 2009, probably more since – was caused largely by a switch from coal to shale gas”. And injecting even more hype, he added that shale gas in the United States “has lowered the price of gas to a quarter of that in Europe, thus slashing the cost of energy, reviving manufacturing, creating jobs, halting the expansion of expensive nuclear power and cutting carbon emissions”.

The EIA’s projections, which assume a rapid increase in shale gas production over the next 25 years, indicate that emissions of carbon dioxide from electricity generation in the United States would be 112 million tonnes, or 4.9 per cent, higher in 2035 compared with 2010, while energy-related emissions would be 172 million tonnes, or 3.1 per cent, greater. Such figures are hardly compatible with emissions reductions of 80 per cent by 2050 that would be required if the United States is to play its part in helping the world to have a reasonable chance of avoiding global warming of more than 2°C.

Shale gas and other natural gas reserves, production and consumption in the UK

So what is the potential for shale gas to have the same impact in the United Kingdom as in the United States?

UK gross annual production of natural gas peaked at 115 billion cubic metres in 2000, but subsequently declined steadily, reaching 60 billion cubic metres in 2010. In 2011, UK gross production of natural gas fell a further 20.8 per cent, to a level lower than annual gross imports for the first time since 1967.

In 2010, 41.3 per cent of the UK’s primary demand for energy was supplied by natural gas. UK total demand for natural gas was about 99.1 billion cubic metres, up from 91.5 billion cubic metres in 2009. Net imports supplied 37.8 per cent of this demand in 2010.

The UK has been a net importer of natural gas since 2004. The increasing reliance on imports of natural gas has had a major impact on fuel bills for households and businesses. Last year, in response to false claims by some campaign groups (including the Global Warming Policy Foundation) and parts of the media that climate change policies were mainly responsible for recent rises in gas and electricity prices, the regulator Ofgem published a report concluding: “Higher gas prices have been the main driver of increasing energy bills over the last eight years”. It pointed out that “Britain enjoyed a period of falling gas prices until 2004/05”, noting that “[t]his is the year that Britain first imported more gas than it produced itself”. It added: “Becoming more reliant on imported gas has meant that British gas prices have become increasingly influenced by global events, especially those that affect the oil prices as often European gas prices are linked to the oil price”.

Any successful exploitation of natural gas reserves from shale could reduce the UK’s dependence on imports. Total UK (onshore and offshore) reserves of natural gas were estimated to be 781 billion cubic metres at the end of 2010. Current estimates indicate the UK has far lower potential onshore reserves of shale gas than the United States. A report for the Department of Energy and Climate Change in 2010 by the British Geological Survey estimated that potentially recoverable onshore reserves of shale gas could be as much as 150 billion cubic metres, which is equivalent to less than two years of UK demand for natural gas. It is not clear to what extent there is offshore shale gas that could also be exploited by the UK.

However, there are also a number of issues that need to be resolved about how easy it will be to extract shale gas safely and economically from onshore reserves in the UK.

Potential risks from shale gas extraction

The British Geological Survey has highlighted a number of environmental risks that need to be managed, and a report in April 2012 commissioned by the Department of Energy and Climate Change identified ways in which the threat of minor earthquakes caused during the extraction of onshore shale gas could be reduced.

One important risk is that fugitive emissions of methane will escape during extraction. This is particularly crucial in terms of climate change because methane has a global warming potential that is 21 times that of carbon dioxide over a 100-year period. It is currently uncertain what volume of fugitive methane emissions escapes during shale gas production. The United States Environmental Protection Agency estimates that about 15.2 billion cubic metres of methane escaped from natural gas systems (including field production, processing, transmission and storage, and distribution) and were emitted to the atmosphere in the United States in 2010, equivalent to about 2.0 per cent of the total dry production of natural gas. However, higher estimates of the rate of fugitive emissions of methane have also been published.

Potential impact of shale gas on UK greenhouse gas emissions

If fugitive emissions of methane can be limited to a negligible level, could shale gas help the UK to achieve its targets for mitigating climate change? The answer is maybe. Some simple back of the envelope calculations show why.

Atmospheric concentrations of greenhouse gases, not including those being phased out under the Montreal Protocol, are nearly 60 per cent higher than before industrialisation. If the world wants to have a reasonable chance of avoiding warming of the Earth by more than 2°C compared with the global average temperature in the mid-19th century, annual global emissions will need to be reduced from the present level of about 7 tonnes per head of population on average (the global population is currently about 7 billion, and annual global emissions were about 50 billion tonnes of carbon-dioxide-equivalent in 2011) to around 2 tonnes by 2050 (the global population will be about 9 billion and global emissions will need to be less than 20 billion tonnes). At present, the UK emits about 8.8 tonnes per head (the UK population of about 62.5 million emitted 549.3 million tonnes of carbon-dioxide-equivalent in 2011). It is this fundamental objective that provides the basis of the target set in the Climate Change Act to reduce UK annual emissions by 80 per cent by 2050 compared with 1990.

The UK’s path towards the 2050 target is laid out through a series of carbon budgets which set the total greenhouse gas emissions allowed during successive five-year periods. The UK is on track to comfortably meet its first budget of 3018 million tonnes of carbon-dioxide-equivalent for the period between 2008 and 2012. Official figures published by the Department of Energy and Climate Change show that UK emissions were 549.3 million tonnes in 2011. If annual emissions stayed at this level for the next six years, the UK would also be able to meet its second carbon budget of 2782 million tonnes for the period between 2013 and 2017. However, such levels of emissions would far exceed the third budget of 2544 million tonnes between 2018 and 2022.

In 2011, 101 million tonnes of greenhouse gases, or 18.3 per cent of the total, were emitted from the combustion of coal, mainly for electricity generation. According to the Department of Energy and Climate Change, natural gas produces about 44 per cent lower greenhouse emissions per kilowatt-hour of electricity generated than coal. So if, for instance, coal was completely phased out in favour of gas by 2018, total annual emissions would fall to 492.7 million tonnes, assuming emissions from all other sources remained no higher than 2011 levels, allowing the third carbon budget to be met.

However, to meet the carbon budgets beyond 2022, emissions from the burning of oil and gas would have to be curbed much further. For gas, this might mean either that gas-fired power stations would run only intermittently, perhaps as back-up for renewables, or would be fitted with carbon capture and storage technology. But both of these options would reduce the profitability of gas-fired power stations. More detailed analyses have reached similar conclusions. Given that power stations are built to operate for several decades, such constraints have to be taken into account by electricity generators now.

Conclusion: how does the hype compare with robust analysis?

If, and only if, the constraints described in previous sections can be managed, along with other risks such as fugitive emissions, then natural gas, including from shale reserves, can play a central role in meeting the UK’s future energy needs. However, it would obviously be an incredible gamble to assume that it is certain that all these constraints and risks can be managed effectively and affordably, and that we can now abandon, as some are advocating, the development and deployment of renewable energy sources, such as onshore wind farms. As the independent Committee on Climate Change has sensibly pointed out, the preferred mix of energy sources in 2030 is likely to include increased roles for both renewables and natural gas, provided carbon capture and storage proves to be economically viable. It is this kind of robust and rigorous analysis by the Committee, rather than the hyped claims of campaigners, that should be informing decisions about the UK’s energy policy.